But behind the scenes? The books are a mess.

For many growing businesses — especially in service industries, construction, mortgage, and professional services — financial records often fall behind operations. And while messy books may seem like a “back-office problem,” they quietly become one of the biggest growth barriers.

Let’s break down the real cost of messy books — and how you can fix it.

Poor Financial Decisions

When your numbers aren’t accurate, it’s hard to know the true financial position of your business. You may think you’re making more profit than you actually are or miss important expenses. Without reliable data, decisions become guesswork instead of smart business choices.

Cash Stress

If you are running your business on outdated records, it becomes difficult to know who owes you money, which bills are due, and how much cash you really have. This lack of clarity can lead to cash shortages and avoidable stress.

Higher Accounting Costs

Messy books also increase your accounting costs. You spend extra time fixing errors, finding missing transactions, and reconciling accounts. With messy books, even a simple bookkeeping task turns into a long cleanup exercise.

Regular bookkeeping is always more affordable than fixing months or years of mistakes later.

Tax Surprises

Messy books and missed documents often lead to tax season stress. Your deductions are wrong and so are your tax submissions. You end up either underpaying or overpaying your taxes. These issues also increase the risk of penalties and notices.

Accurate books make tax filing faster and smoother.

Lost Business Opportunities

Messy financial records can slow down important business decisions. If your numbers are not clear, you would find it extremely difficult to take strategic decisions for your business and may miss good opportunities.

Increased Risk of Errors

Poor bookkeeping leads to duplicate entries, missed transactions, and wrong classifications. These may look like small errors now but can lead to bigger problems later.

Lower business valuation

If you ever plan to sell your business, bring in investors, or raise capital, your financial records will be closely examined. Buyers and investors don’t just look at revenue — they look at cash flow stability, margins, and financial controls.

If your books are unclear, incomplete, or inconsistent, it reduces confidence in your business and can significantly reduce your valuation.

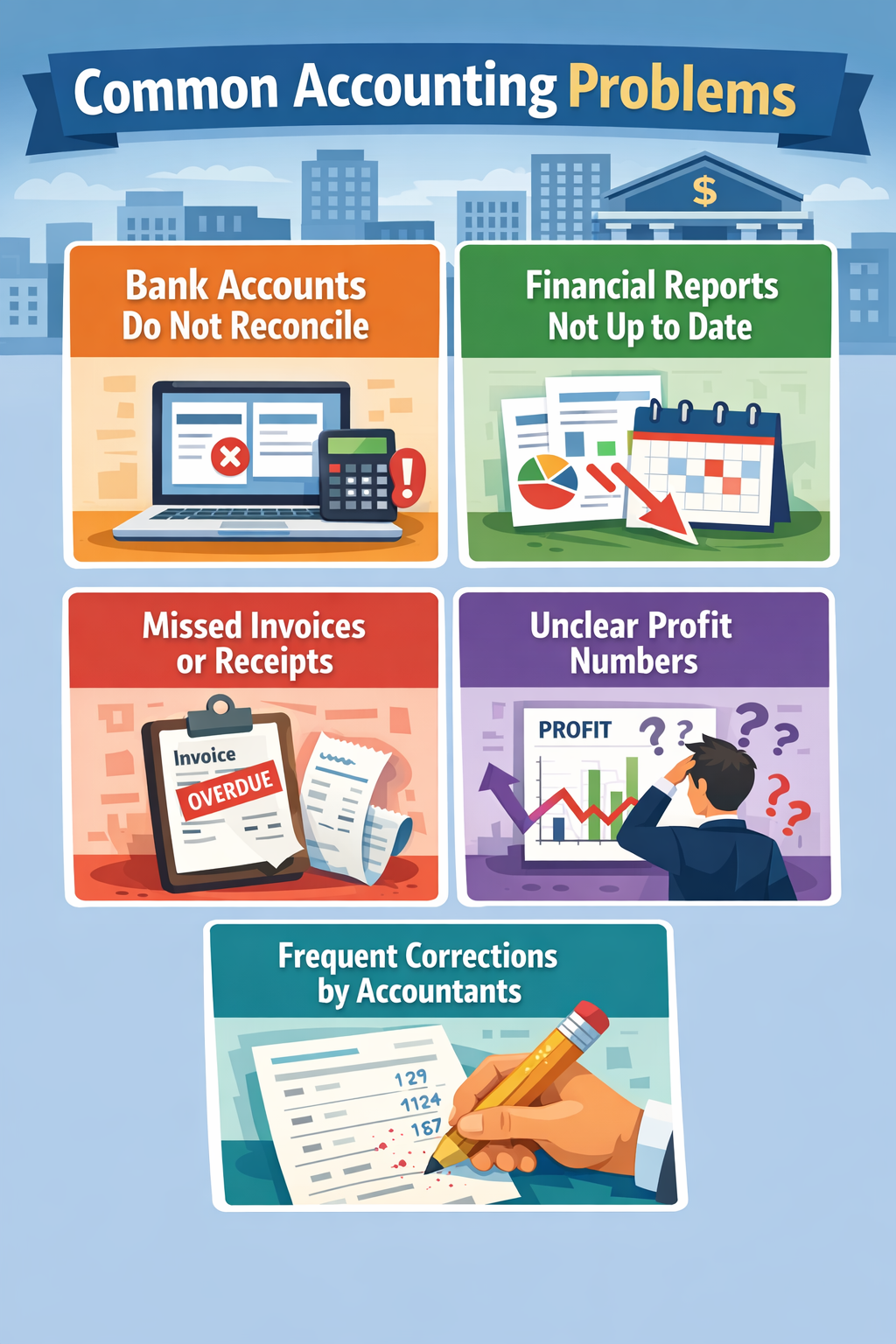

Signs Your Books Need Attention

Some warning signs include:

If any of these signs pertain to your business, your books may need a thorough review or a clean-up.

Why Growing Businesses Struggle With Clean Books

Messy books rarely happen overnight. They build up gradually — often as a side effect of growth.

It usually unfolds in stages:

Stage 1: The Business Is Small

Transactions are limited, and the founder manages daily bookkeeping along with sales, operations, and client delivery. It feels manageable and efficient.

Stage 2: Bookkeeping Is Delegated

As the workload increases, bookkeeping is handed over to a junior employee or part-time resource. The focus remains on recording transactions — not on building financial systems or reporting discipline.

Stage 3: Growth Accelerates

Soon, the revenue multiplies, payroll expands, and financial complexity increases.

But with one junior resource handling the entire back office, processes remain basic.

- Financial reports are delayed.

- Bank accounts aren’t reconciled on time.

- Cash flow visibility becomes unclear.

Growth changes the complexity of finance. If systems don’t evolve with growth, financial clarity weakens. And that gap is where messy books begin.

Practical Steps to Get Your Books Back on Track

Fixing messy books does not always require a complete overhaul. By following some simple steps, you can easily bring your financial records back in order and maintain them going forward.

Here are some practical steps to help you get started:

Update Your Historical Records

The first step is catch up bookkeeping. To reconcile your accounts, you need to first bring your books up to date. Review your past financial data and record any missing entry, so that your reports reflect the true financial position of your business.

Reconcile Your Accounts

Reconcile your bank and credit card accounts to identify any missed entry and errors. Regular reconciliation ensures your financial records match up with your actual balances.

Organize Supporting Documents

Keep all the invoices, receipts, and financial documents properly stored. Good documentation habits help in good bookkeeping and simplifies tax filing.

Use Reliable Accounting Systems

Use a good cloud-based accounting software to reduce efforts and improve accuracy. Technology makes it easy for you to track income, expenses, and financial performance regularly.

Build a Monthly Close Process

Cleaning up your books just once is not enough. It is a continuous process and consistency is key. Review your Profit & Loss, Balance Sheet, and Cash Flow statement every month.

A simple monthly bookkeeping routine ensures all your accounts are reconciled, transactions are reviewed, and financial reports are generated on time.

This small discipline keeps your books accurate, improves financial clarity, and prevents small issues from turning into bigger problems.

Move From Bookkeeping to Financial Visibility

Bookkeeping just tells you what happened. But financial visibility? It helps you decide what to do next.

So, as your business grows, just recording transactions and reconciling accounts is not enough. You need financial insights for effective decision-making.

Analyze your numbers. Make sure you have a:

- A monthly Profit & Loss statement with margin analysis

- A rolling cash flow forecast

- Budget vs. actual comparisons

- Department or branch-level profitability

- Clear performance indicators (KPIs)

Remember, numbers alone don’t create clarity. You need real-time analysis to turn those numbers into strategic direction.

Separate Transaction Work from Financial Oversight

A common mistake in growing businesses is expecting one person to handle everything. In long term, this doesn’t work.

As complexity increases, your business needs layered financial support. So, invest in upgrading your financial systems and processes to match your growth.

Get Professional Support When Needed

If you have not updated your books for a long time, hire a professional bookkeeper to correct errors and establish a reliable system for the future. A professional can help identify gaps, fix past mistakes, and ensure your financial records are accurate and up to date.

Clean and accurate books not only reduce stress but also support better business decisions and long-term growth.

It’s Time to Turn Your Messy Books into Clean Accurate Records

Messy books rarely cause immediate damage, which is why they are often ignored. But the hidden costs add up over time and lead to serious financial consequences.

Invest in proper bookkeeping system today to prevent expensive problems in the future. Partner with our expert bookkeepers to bring clarity and structure back into your business. We correct your past errors and help you maintain accurate books going forward.

With clean and reliable financial records, you can make better decisions, stay compliant, and focus on growing your business with confidence.